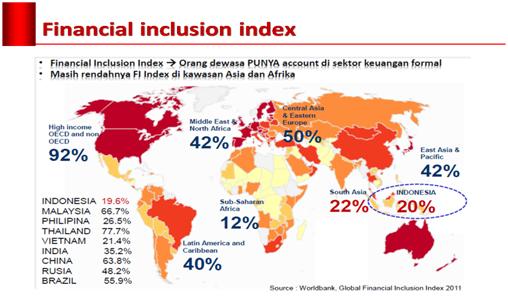

[caption caption="Financial Inlusion Index (doc: WB Global Financial Inclusion Index 2011)"][/caption]

Financial inclusion has been an important policy goal for quite some time. However, to date a sizeable majority of the population, especially the poor and vulnerable people still have no access to financial services. This is due to limited availability and accessibility of financial services.

Social benefits could be obtained if access to financial services could be improved. If the entire population have access to financial services, the government could distribute cash subsidies directly to the recipient's account. Therefore there are no long queues for the distribution of the cash subsidies would no longer occur. As a result, financial inclusion makes people, especially the poor, connected with economic opportunities. Thus it’s fostering economic growth and individual welfare.

This is just an example of how financial inclusion can benefit people who are currently not connected into the financial system. Hence, formidable tasks lie ahead.

The Challenge of Financial Inclusion

Financial inclusion defines as the right of every individual to have access to a full range of quality financial services in a timely, convenient, informed manner and at an affordable cost. So, in here financial services are provided to all segments of the society, with a particular attention to low income poor, productive poor, migrant workers and people living in remote areas. As a result, provide financial services and products need comprehensive financial inclusion strategy that are able to address all the different needs arising from different segments of the population and do so through a holistic set of services.

This strategy aims to address all layers of the population but with a clear understanding that different layers have different social and financial needs. However, it explicitly targets those groups with the greatest need or unmet demand for financial services and making sure that all key segments are taken into consideration. So, overcoming the barriers will create a fundamental breakthrough in simplifying access to financial services. In other word, Know Your Customers are needed for small value customers. All these things need to be done without compromising the principle of stability and prudent banking.

Therefore, the most important for the conceptual terms for inclusion should be. “Simplicity and reliability in financial inclusion, though not a cure all, can be a way of liberating the poor from dependence on public services. Further, the products should address their needs — a safe place to save, a reliable way to send and receive money.”

According to Global Index data 2014, there are 2 billion people that don’t use formal financial services and more than 50% of adults in the poorest households are unbanked. The reason for these is because of costs, travel distances and the often burdensome requirement involved in opening account. Therefore, financial inclusion is a key enabler to reducing poverty and boosting prosperity. As the World Bank President Kim has called for Universal Financial Access (UFA) by 2020.

In Indonesia the financial system is dominated by banks. The total of financial asset, banks manage 79 per cent as the World Bank Report in 2010. However most of the banks are present in densely populated areas, which are closely associated with the volume of economic activity that is in Java and more than 400 cities across Indonesia do not have bank branches. As a result, the banking sector is concentrated in and around Jakarta while low population and remote districts tend to be underserved.

Therefore there is a need for synergy to be developed between the strategy for increasing access of financial services and economic development programs, as well as, poverty reduction efforts. Taken together, the above findings underscore the importance of expanding financial service institutions abilities to offer both savings and credit services, while raising depositors’ incomes through broader policies of economic development. These findings also underscore the challenge for Indonesia’s formal financial system to expand its client base and to reach a much larger portion of the population.

Therefore the banking sector will remain backbone of financial inclusion. Bank will continue to play a major role in the provision of financial services. For this reason it’s important to see how the branch networks can be strengthened and expanded to reach greater proportion of population.

Moreover with the help of technology can enable some of the most important bottlenecks to overcome and increase the supply of financial service. Through technology consumers can carry out banking without ever stepping into a bank. This convenience can be great incentives for consumers to have a bank account. Information and Communication Technology can also reduce transaction costs and expand the formal financial system outreach in regards to saving and loan services.

As a result branchless banking in the form of mobile phone banking (i.e. mobile money), internet banking or transaction using a card or electronic machine are technological breakthrough with huge potential for extending the coverage of financial service to consumers who are not yet served by the banking sector.

The good thing is there is high access of Indonesians residents to cellular telephone technology makes it very convenient to increase access to financial services through the technology. This innovation could be combined with-money services, utilizing retail networks as outlets for banks.

[caption caption="BCA and Indepay Network signings (doc: Ben B. Nur)"]

Launching Low-cost Payment Network through Local Agents

For this reason one of the biggest private bank in Indonesia known as Bank Central Asia (BCA) takes commitments to improve the services for the people living in rural and less populated areas. They intend to strengthen the financial inclusion with this recent plan known as branchless banking system. As we all know throughout the years BCA has held an impactful stance upon Indonesia’s economy in banking.

In this attempt to connect to the customers through branchless banking system, BCA has paired up with Indepay Network, accompany that have based in Singapore and specializes in doing such. Both companies have signed a cooperation agreement to launch Low-cost Payment Network. Previously Indepay has been operating in India since 2007 with aims of easing up the transaction process through a payment network.

The collaboration of the two companies was done on Monday the 21th of December 2015 when Indepay signed a Cooperation Agreement at the BCA Building Nusantara on Jalan Thamrin Jakarta. The BCA was represented by the Director of BCA, Suwignyo Budiman and Indepay Network represented by Rajib Saha, the CEO of Indepay Network. This signing agreement was also witnessed by Independent Commissioner of BCA, Cyrillus Harinowo; BCA Director, Henry Koenaifi and Vice President of Indepay Network, John Lee.

In his speech after the signing of the cooperation, Suwignyo explained that BCA and Indepay has long been exploring each other to ensure that this cooperation can provide maximum benefits for BCA customers in Indonesia. During the signing Suwignyo discussed about plans for a pilot Project to take place a small trial for testing services through branchless banking with the use of agents in Grobogan, Central Java and Cigugur West Java.

So far BCA has long focused on their services in urban areas while Indepay is effective in providing support without the usage of bank branches. Rajib Saha also said that transactions can be made without having to travel far from their (customer) homes. Although it is true that having personal agents can be costly, the services will make up for the relatively small cost, replied Suwignyo when asked on the matter.

BCA also plans to implement Kartu Layanan shortened as LAKU to reduce possible technological errors and for ease of use among the community. Suwignyo plans to spread Kartu LAKU throughout all of Indonesia.

[caption caption="Post Signings the Agreement (doc: Ben B. Nur)"]

Follow Instagram @kompasianacom juga Tiktok @kompasiana biar nggak ketinggalan event seru komunitas dan tips dapat cuan dari Kompasiana

Baca juga cerita inspiratif langsung dari smartphone kamu dengan bergabung di WhatsApp Channel Kompasiana di SINI