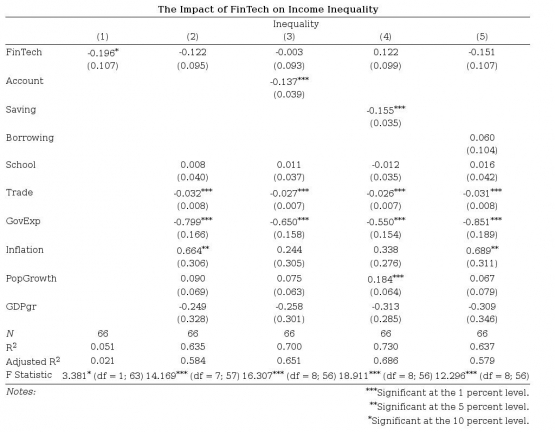

Econometric Results

Figure 1.7 presents the fixed effect regression results for income inequality. The first two columns show the regression on fintech only, then fintech with control variables, respectively. From the first column, fintech is correlated significantly with inequality, negatively, at 10% significance level. However, when control variables are added, fintech’s negative correlation becomes insignificant. In column (3)-(5), we included additional variables for financial inclusion (account, saving, borrowing) into the regressor that was regressed individually.

Column (3) presents the results for when account is added into column (2). Estimated coefficient for account is significant at 1% significance level and negatively correlated with inequality. Though fintech estimated coefficient reduced from -0.122 to -0.003, it can’t be concluded yet that fintech affects inequality through an intermediary of account ownership at a formal financial institution as the result in column (3) is insignificant.

Column (4) exhibits results after adding saving into column (2). The result shows that saving is negatively correlated with inequality at 1% significance level. However, fintech shows an insignificant positive correlation with inequality which differs from Demir et al. (2020) results.

Column (5) displays the result for estimation when borrowing is added to column (2). Here, borrowing shows an insignificant positive correlation with inequality whereas fintech also shows insignificancy, but negative correlation with inequality. Having shown anomaly compared to Demir et al. (2020) results, our findings implies that financial inclusion is still debatable regarding its importance in being an intermediary through which fintech adoption affects income inequality.

In general, significantly, financial inclusion in terms of account and saving show negative correlation with inequality whereas financial inclusion in terms of borrowing show otherwise. Our result on borrowing is not in line with Demir et al. (2020) as their findings prove a negative correlation. Regarding magnitude, it can be interpreted that a one point increase in fintech adoption will; reduce income inequality by 0.003 when adding account, increase income inequality by 0.122 when adding saving, and reduce income inequality by 0.151 when adding borrowing, though more samples are needed as none result show significance. Moreover, our overall model shows a jointly significant correlation with inequality as all of the F-test are proven to be significant. Control variables also behave largely as expected in Demir et al. (2020) results which indicate that our control variables play a significant role in reducing income inequality.

In conclusion, proxied with mobile phone used to pay bills (% age 15+), fintech affects inequality, proxied with Gini coefficient, negatively and significantly. However, when financial inclusion variables (formal account ownership, savings, and borrowings) are added individually, the relationship becomes insignificant, and even positive for saving. This indicates that fintech is still uncertain in affecting inequality through financial inclusion as more samples are needed.

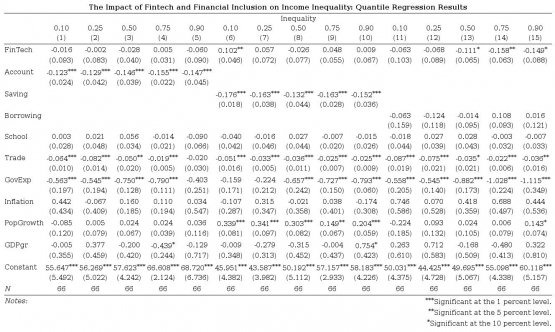

Having shown that fintech has inequality-reducing effects, we are now going to examine this effect for countries at different levels of inequality. Figure 1.8 shows our quantile regression results for 33 OECD countries when using the three different proxies of financial inclusion. In columns (1) to (5), the variable account is used as a proxy for financial inclusion, where the signs of the coefficients on accounts are negative at all quantiles, which is consistent with our results in Figure 1.7. Thus, at all quantiles of the inequality distribution, an increase in the proportion of the population owning an account at a formal financial institution is associated with a reduction in inequality. Although the coefficient signs are in line with Demir et al. (2020), the magnitudes of the inequality-reducing effects slightly differ. In the original study, the effect of formal account ownership on inequality strictly increases as we move up to higher inequality quantiles. In our findings, the effect only increases up until the 75th percentile, after which the coefficient decreases in magnitude. Given all account coefficients are significant at the 1% level, we can reject the null hypothesis that all regression quantile coefficients on account are equal. However, given the coefficients on fintech are not statistically significant, we could not conclude that mobile payments have inequality-reducing effects when account ownership is used as a proxy for financial inclusion.

In columns (6) to (10), we proxied financial inclusion using the variable saving, in which the coefficients on saving are negative at all quantiles. This is consistent with figure 1.7, verifying that formal saving does have inequality-reducing effects at all quantiles. However, unlike the original study, formal savings does not increasingly reduce inequality in more unequal countries. Rather, our results show that formal savings reduce inequality the strongest at the 10th percentile, and the least strong at the 50th percentile. Given the coefficients are all significant at the 1% level, we can reject the null hypothesis that all regression quantile coefficients on saving are equal. For our findings on FinTech, only the 10th quantile was statistically significant, where we found that 1-percentage point increase in mobile payments leads to a 0.102-percentage point reduction in income inequality.